Establishing new homes in disaster hazard zones could value billions, threaten affordability

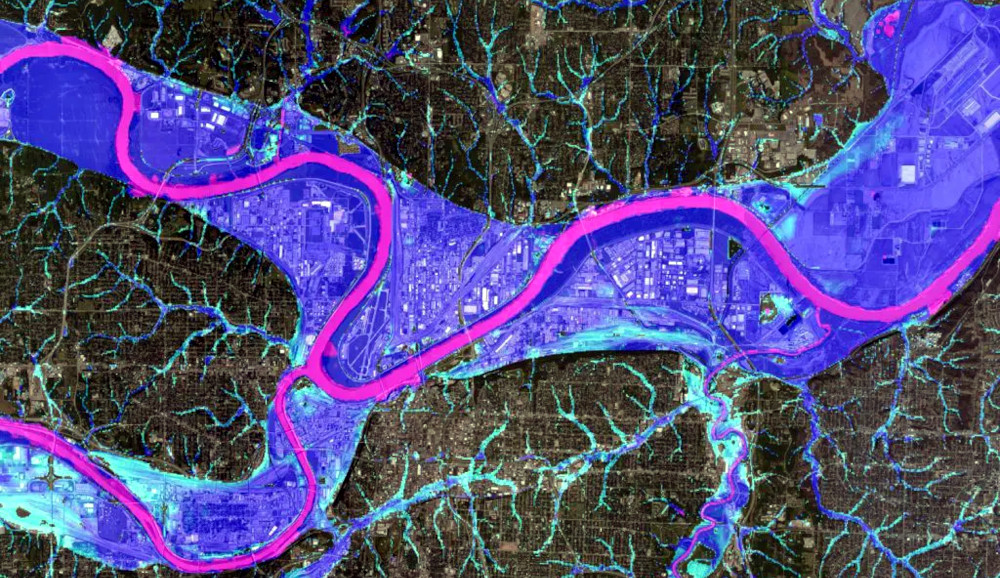

Image credit score rating: Fathom

Image credit score rating: Fathom

Worldwide

As is the case in most developed worldwide places, governments all through Canada are

racing to assemble additional housing to boost affordability. However a model new study from the

Canadian Native climate

Institute

has found these efforts risk putting an entire lot of 1000’s of homes in damage’s

method — and together with billions of {{dollars}} in costs yearly — besides protection is

improved to direct enchancment away from the specter of wildfires and floods.

As Close to Dwelling: The suitable approach to assemble additional housing in a altering

native climate

outlines, developing new homes in areas at a extreme risk of flood or wildfire could

value governments, insurers and house owners as a lot as $3 billion additional yearly for

rebuilding and disaster help. These risks are neither distant nor abstract:

Damages from merely 4 extreme-weather events in July and August 2024 —

flooding

in Toronto and Southern Ontario, the catastrophic

wildfire

in Jasper, extreme

flooding

in Quebec and an historic

hailstorm

in Calgary — totaled higher than $7 billion in insured

losses.

One of many essential putting findings of the study is that plenty of the projected

costs are associated to a relatively small number of homes anticipated to be

in-built flood-vulnerable zones: Redirecting merely three % of newest homes

away from the highest-risk flood areas could save virtually 80 % of all

projected weather-related losses by 2030.

“Basically probably the most cheap home is the one you should not have to rebuild after a disaster.

Governments all through Canada can save billions of {{dollars}} yearly and protect people

protected against disasters by developing solely a small proportion of newest homes away from

the highest-risk areas for wildfires and floods,” says Ryan

Ness, Director of Adaptation

on the Canadian Native climate Institute. “Our new report outlines the devices

policymakers must steer new housing to safer flooring and help affordability

inside the course of.”

The report — which contains wildfire-risk analysis from Canadian financial

corporations company Co-operators, flood-risk modeling

by Fathom Worldwide and future housing risk analysis

by SSG — is a first-of-its-kind analysis in Canada to model

the financial costs of future floods and fires on new housing slated for

constructing by 2030.

It finds that higher than 540,000 homes could very properly be in-built areas of flood hazard

and higher than 220,000 homes in locations uncovered to extreme wildfire hazards by

2030. The associated full costs usually tend to be highest in British

Columbia — which faces $2.2 billion in added annual costs beneath a worst-case

state of affairs — adopted by Manitoba ($360 million), Alberta ($220

million), and Quebec ($214 million). The Yukon may even see will improve in

frequent damages as extreme as $1,200 for each new dwelling from flooding alone, successfully

previous the nationwide frequent.

The Native climate Institute moreover commissioned a companion report, Indigenous

Housing and Native climate

Resilience,

by Shared Value

Choices

to ascertain distinctive challenges and obstacles confronted by Indigenous Nations in

rising climate-resilient homes, with a particular focus on housing on First

Nations reserves. The report examines worthwhile insurance coverage insurance policies and practices, and

presents 9 protection strategies.

“Fixing Canada’s housing catastrophe requires not merely developing additional homes nonetheless

making sure they’re cheap in the long term. This accommodates developing new homes

in protected locations which may be resilient to increasingly more excessive floods and

wildfires,” asserts Lisa Raitt,

Vice-Chair of Worldwide Funding Banking at

CIBC and Co-Chair of the Exercise Stress for

Housing and Native climate. “This new Native climate Institute

report highlights the financial risks Canada faces if housing protection continues

to allow harmful enchancment, and affords actionable choices to protect people

and property.”

The report notes that each one ranges of presidency have a job to play in decreasing

the threats of most local weather disasters to new homes, and affords these protection

strategies:

-

Federal, provincial and territorial governments must steer housing and

infrastructure funding away from high-hazard zones to low-hazard areas. -

Provincial and territorial governments must strengthen land use protection to

redirect new constructing away from areas at extreme risk of flood and fireside

damage. -

Federal, provincial and territorial governments must reform

disaster-assistance packages to discourage harmful enchancment — as an example, by

making new homes in-built high-hazard zones ineligible for publicly funded

disaster compensation. -

Governments must create, protect and make publicly on the market maps that

current hazardous areas — and mandate the disclosure of such knowledge in

precise property transactions — so that house owners, renters and builders have

entry to that info. -

The federal authorities must empower and help Indigenous communities to

assemble climate-resilient

homes

in safer areas inside their territories.

“Native governments, on the forefront of every the native climate and housing crises, are

vital companions in safeguarding Canadians and defending communities from

escalating native climate impacts,” says Carole

Saab, CEO of Federation of Canadian

Municipalities. “This report highlights the urgency of coordinating all through all

orders of presidency and sectors to take care of Canadians and their homes protected against

increasingly more excessive wildfires and floods.”

Native weather-driven migration, insurance coverage protection will improve could erase $1.4T in US precise property price by 2055

The LA fires, January 2025 | Image credit score rating: Maxar

The LA fires, January 2025 | Image credit score rating: Maxar

Within the meantime, First Avenue’s just-released twelfth

nationwide report estimates a doable $1.47 trillion low cost in US precise

property price over the following 30 years ensuing from climate-related risks.

First Avenue makes use of clear, peer-reviewed methodologies to quantify the earlier,

present and future native climate risk for properties globally and makes it on the market

for residents, enterprise and authorities. In October, Zillow began offering

First Avenue’s data for five key climate-related

risks

on all for-sale property listings all through the US — serving to patrons to raised

assess long-term affordability and plan for the long term.

Drawing on interdisciplinary evaluation that examines native climate risk consciousness,

housing market dynamics, native climate migration patterns, and demographic and

socioeconomic shifts, First Avenue’s new Property Prices in

Peril report

affords a forward-looking analysis of the Housing Value

Index,

property-valuation developments and localized GDP impacts extending to 2055.

Key findings

-

By 2055, climate-driven local weather phenomena are anticipated to increase home-owner

insurance coverage protection premiums nationwide by a median of 29.4 % — the 5

largest metro areas going by the most effective insurance coverage protection premium will improve are Miami

(322 %), Jacksonville (226 %), Tampa (213 %), New Orleans

(196 %), and Sacramento (137 %). -

Concurrently, migration induced by native climate risks along with extreme heat,

wildfire and flooding is anticipated to drive vital inhabitants

redistribution, with 55 million Folks anticipated to relocate all through the US

over the equivalent interval to historically a lot much less populous states harking back to North

Dakota and Montana — which might be forecasted to develop ensuing from their native climate

resilience.

“Native climate change just isn’t a theoretical concern; it is a measurable strain

reshaping precise property markets and regional economies all through the US,”

acknowledged Dr. Jeremy Porter, Head of

Native climate Implications Evaluation at First Avenue. “Our findings highlight the

urgent wish to know the way rising insurance coverage protection costs and inhabitants actions

are transforming the monetary geography of the nation.”

The study duties a stark divergence in property values: Extreme-risk areas are

extra more likely to experience vital devaluation, whereas areas perceived as

native climate resilient are

poised to revenue from elevated demand. This reallocation of monetary train

could have profound implications for native authorities revenues — with at-risk

areas going by reductions in property tax earnings, whereas additional resilient areas stand

to comprehend.

“These outcomes highlight not solely the pressing challenges however moreover the

options for adaptation and

innovation

inside the face of native climate change,” added First Avenue founder and CEO Matthew

Eby. “Policymakers, corporations and

communities ought to act now to mitigate risks and capitalize on the rising

monetary options in a shifting panorama.”

Get the latest insights, developments, and enhancements to help place your self on the forefront of sustainable enterprise administration—delivered straight to your inbox.

Sustainable Producers Workers

Revealed Feb 7, 2025 8am EST / 5am PST / 1pm GMT / 2pm CET